The presentation to all partners in a VC firm wil decide whether that firm will issue you a term sheet. This pitch is just as important as the pitch you give to the one partner that you have been working together with for the last few months, if not more important. However, the emphasis of the pitch is different to the first pitch that you gave. The partner pitch has to prevent the partners from saying NO, not to make them actively say YES.

This article is part of a series, you can find the Index of the VC Fund Raising Manual here.

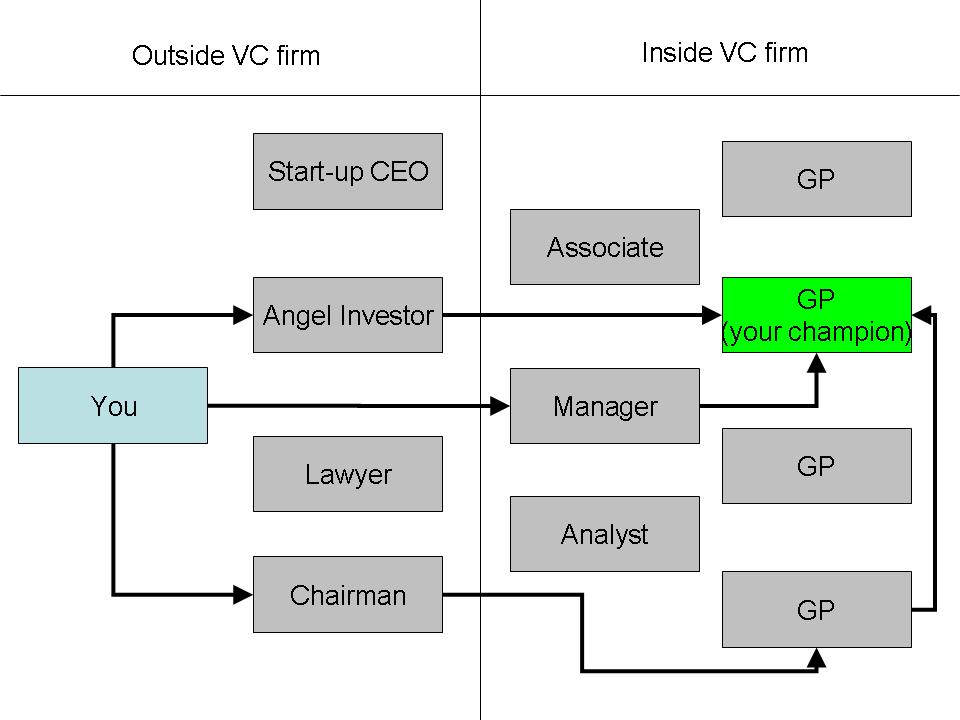

In order to understand why the partner presentation is so important, you need to understand that most VC firms are partnerships. This partnership, an investment partnership, makes the investment decisions as a group. It is extremely common practice that if one partner is really unhappy about a deal, the deal is not done, regardless of what the other partners think.

So, during due diligence, you have made the partner whom you have have been working together with so excited and confident, that now she is happy for you to present to all the other partners. In a sense, she is now your sponsor in that group of people. Also remember that most of the partners will not be experts in your area. The expert is the partner you have been working together with for the last few months. The others are likely to listen to the opinion of the expert in the group, unless they can find some real flaws in what you are pitching.

So, you and your sponsoring partner will walk in the room and you will get to know all the other partners. The partner who is sponsoring you has already been pitching all the other partners about you several times. They are all pretty agreed that the deal you are offering is very exciting. Your job in this pitch is not to convince them that this deal is exciting. They are already excited. Your only job is not to screw it up at this stage. Your job is to prevent one partner vetoing the deal:

So, whatever you do, don’t do any of the following things:

- No surprises. They might not like whatever it is that you pull out of the hat (well, unless it is good news, e.g. “We just closed our first customer” or “The technology works twice as fast and twice as well as we thought”)

- Don’t change your pitch. The partners there are sold on your pitch already, never change the winning story.

- No unnecessary details. Whatever they are, they might not like them. Keep it simple.

Overall, your job is to give the same pitch, removing some of the finer detail, that you gave to the partner who is now sponsoring you.

Focus your attention on the biggest naysayers. One person who dislikes your deal is enough to kill it. Focus your attention on that person and win her over.

Overall, pitching to many partners is like doing a PhD viva. You have already been doing all your work. Your supervisor has proof-read your dissertation and has submitted it with her approval to her peers for peer review. The peers don’t actually need to love your PhD. Or at least not enough to be happy to sponsor it. But if they dislike it, they will make you go back to do some more work. And you really don’t want to do that.

The same is true for VCs. You really don’t want to fail at this stage, after having gone through all the due diligence.

After a successfull partner presentation, the VC firm is likely to offer you a term sheet, which I will talk about in Part 7 of this series. This article is part of a series, you can find the Index of the VC Fund Raising Manual here.

![]()

Subscribe in a Reader

Subscribe in a Reader ![]() Subscribe by Email

Subscribe by Email

{kind=link}